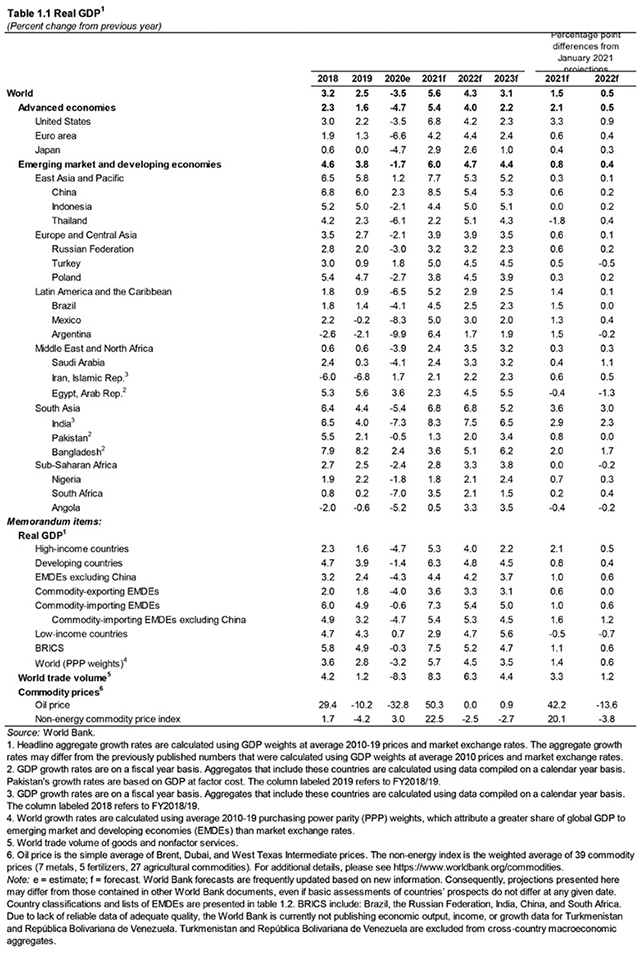

The global economy is expected to expand 5.6% in 2021, the fastest post-recession pace in 80 years, largely on strong rebounds from a few major economies. However, many emerging market and developing economies continue to struggle with the COVID-19 pandemic and its aftermath, the World Bank says in its June 2021 Global Economic Prospects.

Despite the recovery, global output will be about 2% below pre-pandemic projections by the end of this year. Per capita income losses will not be unwound by 2022 for about two-thirds of emerging market and developing economies. Among low-income economies, where vaccination has lagged, the effects of the pandemic have reversed poverty reduction gains and aggravated insecurity and other long-standing challenges.

“While there are welcome signs of global recovery, the pandemic continues to inflict poverty and inequality on people in developing countries around the world,” said World Bank Group President David Malpass. “Globally coordinated efforts are essential to accelerate vaccine distribution and debt relief, particularly for low-income countries. As the health crisis eases, policymakers will need to address the pandemic’s lasting effects and take steps to spur green, resilient, and inclusive growth while safeguarding macroeconomic stability.”

Among major economies, US growth is projected to reach 6.8% this year, reflecting large-scale fiscal support and the easing of pandemic restrictions. Growth in other advanced economies is also firming, but to a lesser extent. Among emerging markets and developing economies, China is anticipated to rebound to 8.5% this year, reflecting the release of pent-up demand.

Emerging market and developing economies as a group are forecast to expand 6% this year, supported by higher demand and elevated commodity prices. However, the recovery in many countries is being held back by a resurgence of COVID-19 cases and lagging vaccination progress, as well as the withdrawal of policy support in some instances. Excluding China, the rebound in this group of countries is anticipated to be a more modest 4.4%. The recovery among emerging market and developing economies is forecast to moderate to 4.7% in 2022. Even so, gains in this group of economies are not sufficient to recoup losses experienced during the 2020 recession, and output in 2022 is expected to be 4.1% below pre-pandemic projections.

Per capita income in many emerging market and developing economies is also expected to remain below pre-pandemic levels, and losses are anticipated to worsen deprivations associated with health, education and living standards. Major drivers of growth had been expected to lose momentum even before the COVID-19 crisis, and the trend is likely to be amplified by the scarring effects of the pandemic.

Growth in low-income economies this year is anticipated to be the slowest in the past 20 years other than 2020, partly reflecting the very slow pace of vaccination. Low-income economies are forecast to expand by 2.9% in 2021 before picking up to 4.7% in 2022. The group’s output level in 2022 is projected to be 4.9% lower than pre-pandemic projections.

An analytical section of the Global Economic Prospects report examines how lowering trade costs such as cumbersome logistics and border procedures could help bolster the recovery among emerging market and developing economies by facilitating trade. Despite a decline over the past 15 years, trade costs remain almost one-half higher in these countries than in advanced economies, in large part due to higher shipping and logistics costs. Efforts to streamline trade processes and clearance requirements, to enable better transport infrastructure and governance, encourage greater information sharing, and strengthen competition in domestic logistics, retail, and wholesale trade could yield considerable cost savings.

“Linkages through trade and global value chains have been a vital engine of economic advancement for developing economies and lifted many people out of poverty. However, at current trends, global trade growth is set to slow down over the next decade,” World Bank Group Vice President for Equitable Growth and Financial Institutions Indermit Gill said. “As developing economies recover from the COVID-19 pandemic, cutting trade costs can create an environment conducive to re-engaging in global supply chains and reigniting trade growth.”

Another section of the report provides an analysis of the rebound in global inflation that has accompanied recovering economic activity. The 2020 global recession brought about the smallest inflation decline and the fastest subsequent inflation upturn of the last five global recessions. While global inflation is likely to continue to rise over the remainder of this year, inflation is expected to remain within target ranges in most inflation-targeting countries. In those emerging market and developing economies where inflation rises above target, a monetary policy response may not be warranted provided it is temporary and inflation expectations remain well-anchored.

“Higher global inflation may complicate the policy choices of emerging market and developing economies in coming months as some of these economies still rely on expansionary support measures to ensure a durable recovery,” World Bank Prospects Group Director Ayhan Kose said. “Unless risks from record-high debt are addressed, these economies remain vulnerable to financial market stress should investor risk sentiment deteriorate as a result of inflation pressures in advanced economies.”

Rising food prices and accelerating aggregate inflation may also compound challenges associated with food insecurity in low-income countries. Policymakers in these countries should ensure that rising inflation rates do not lead to a de-anchoring of inflation expectations and resist subsidies or price controls to avoid putting upward pressure on global food prices. Instead, policies focusing on scaling up social safety net programs, improving logistics and climate resilience of local food supply would be more helpful.

Regional Outlooks:

East Asia and Pacific: Growth in the region is projected to accelerate by 7.7% in 2021 and 5.3% in 2022. For more, see regional overview.

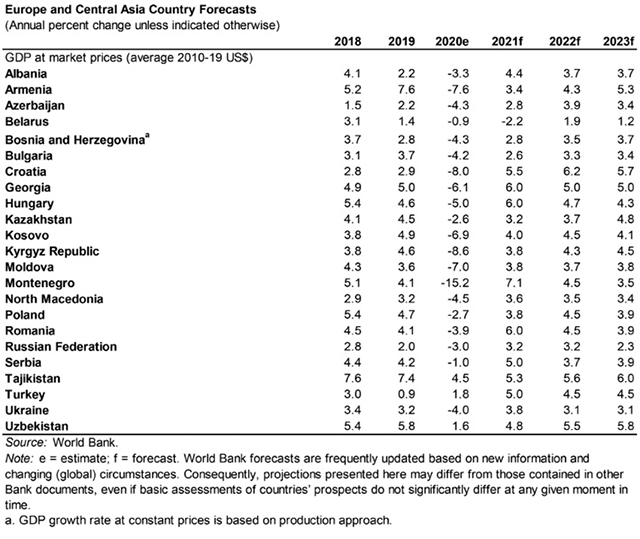

Europe and Central Asia: The regional economy is forecast to grow by 3.9% this year and 3.9% next year. For more, see regional overview.

Latin America and the Caribbean: Regional economic activity is expected to grow by 5.2% in 2021 and 2.9%. For more, see regional overview.

Middle East and North Africa: Economic activity in the Middle East and North Africa is forecast to advance by 2.4% this year and 3.5% next year. For more, see regional overview.

South Asia: Economic activity in the region is projected to expand by 6.8% in 2021 and 6.8% in 2022. For more, see regional overview.

Sub-Saharan Africa: Economic activity in the region is on course to rise by 2.8% in 2021 and 3.3% in 2022. For more, see regional overview.

Global Economic Prospects: Europe and Central Asia

The region continues to grapple with COVID-19. After declining in early 2021, cases accelerated as new variants emerged and population mobility increased. The vaccination progress has been uneven across the region. The resurgence of COVID-19 cases in early 2021 has weighed on the incipient economic recovery; manufacturing has faltered; and services activity remains subdued.

Recent currency depreciations have put further upward pressure on prices. Nearly half of the central banks of the region that have inflation targets contended with inflation levels that exceeded the upper limits in early 2021, and policy rates have been raised in several countries. Fiscal support packages enacted to address the economic shock associated with the pandemic are expected to be partially unwound this year. Due to the large fiscal response and last year’s contraction in output, median public debt is expected to be 54% of GDP by end-2022, nearly 15 percentage points higher than in 2019. However, targeted fiscal support is estimated to have averted a large spike in poverty and job losses.

Outlook

The regional economy is forecast to expand a stronger-than-expected 3.9% in 2021, partly due to improvement in the euro area. However, the outlook remains challenging given the recent worsening of the pandemic, tighter macroeconomic policy, and elevated policy uncertainty and geopolitical tensions. The forecast is predicated on a faster pace of vaccination in the second half of the year in the region’s largest economies. Growth is expected to stabilize at 3.9% in 2022. However, per capita GDP in 2022 is forecast to be 5.3% below the level expected prior to the pandemic.

Growth in Russia, the region’s largest economy, is projected to reach 3.2% in 2021, supported by firming domestic demand and elevated energy prices. Tighter-than-expected macroeconomic policy and an escalation of geopolitical tensions in 2021 are weighing on the outlook. Growth is expected to remain steady at 3.2% in 2022. In Turkey, the second largest economy in the region, growth is projected to rise to 5% in 2021, as exports benefit from firming external demand, before moderating to 4.5% in 2022.

In Central Europe, growth is projected at 4.6% in both 2021 and 2022, supported by a recovery in trade. Exceptional policy accommodation is expected to continue through 2021, and sizeable EU fund packages for member states should help mitigate weakness in investment. Growth in the Western Balkans is forecast to rebound to 4.4% this year and moderate to 3.7% in 2022, assuming consumer and business confidence revives as vaccination takes place and political instability eases. The South Caucasus is projected to return to growth in 2021, expanding 3.6% and strengthening to 4.2% in 2022, predicated on dissipation of shocks related to the pandemic and to conflict.

Eastern Europe is projected to expand 1.9% in 2021 and 2.8% in 2022, as the recovery is constrained by geopolitical tensions, subdued domestic demand, and structural weakness. Growth in Central Asia is forecast to recover to 3.7% in 2021 and 4.3% in 2022, supported by a modest rise in commodity prices, relaxation of production cuts among major oil producers, and increased foreign direct investment.

Risks

Risks to the outlook are tilted to the downside. Although the region has had some success in administering the vaccine in some countries – mainly in Central Europe, the Western Balkans, and Turkey – deployment elsewhere has lagged. The pandemic could also add a further drag to already slowing investment in human and physical capital. Financial stress is another risk to the outlook. Intensifying geopolitical tensions or further rises in policy uncertainty pose additional downside risks in the region.

World Bank Group COVID-19 Response

Since the start of the COVID-19 pandemic, the World Bank Group has committed over $125 billion to fight the health, economic, and social impacts of the pandemic, the fastest and largest crisis response in its history. The financing is helping more than 100 countries strengthen pandemic preparedness, protect the poor and jobs, and jump start a climate-friendly recovery. The Bank is also providing $12 billion to help low- and middle-income countries purchase and distribute COVID-19 vaccines, tests, and treatments.